Investors evaluating Michael Saylor's MicroStrategy (MSTR) may be overlooking a critical capital market measure: amplification. This metric compares the company's total debt and preferred stock to its Bitcoin holdings. As amplification increases, it introduces higher risk, making MSTR's common stock more sensitive to Bitcoin's price fluctuations.

While focus has been on Bitcoin's price and MicroStrategy's net asset value (NAV) premium, rising amplification could become the dominant risk factor. The company carries approximately $8.25 billion in convertible debt, its most senior claim. Below this are preferred stocks, including STRC, STRK, STRD, and STRF, with a notional value around $10.3 billion. Common equity (MSTR) absorbs all remaining residual risk and reward.

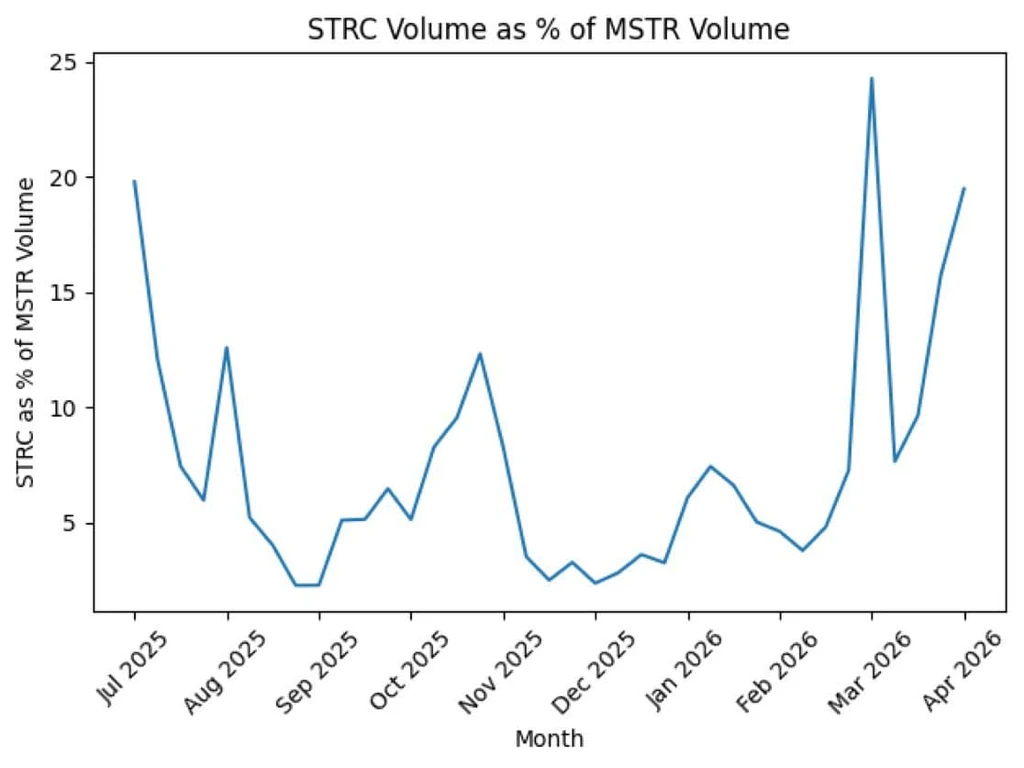

STRC has become a primary vehicle for MicroStrategy's Bitcoin accumulation. This preferred stock, senior to equity but junior to debt, pays an 11.5% annual dividend. Recently, STRC trading volumes have surged, occasionally reaching 20-25% of MSTR's weekly volume. This increased activity makes managing amplification more challenging without relying on common stock issuance, which can dilute performance against Bitcoin.

At lower amplification levels, MSTR typically acts like leveraged Bitcoin. However, at higher levels, managing the strategy becomes more complex, compounded by roughly $1.12 billion in annual financial obligations.