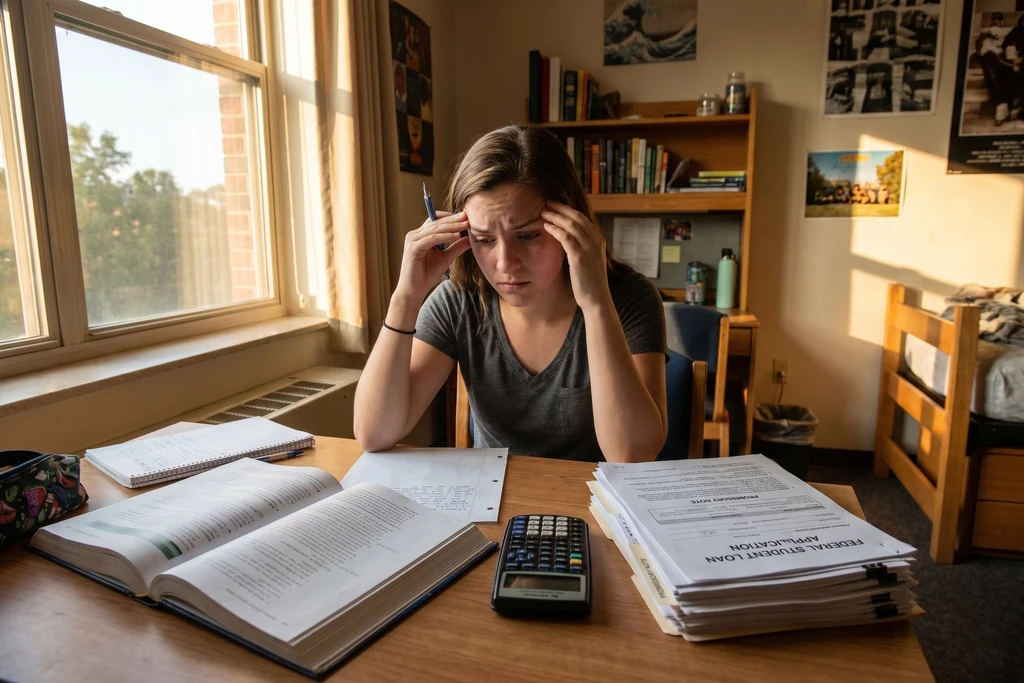

Federal student loan rates are edging higher for the 2026-27 academic year. The 10-year Treasury yield used to set these rates rose to 4.47% in May, pushing undergraduate loans to an expected 6.52%, graduate loans to 8.07%, and Parent PLUS loans to over 9%. Experts say that while the increase is modest-about 10 basis points-it still adds to the cost of education.

For undergraduate students, federal loans remain a favorable first option, offering capped amounts and federal protections. However, for graduate and Parent PLUS loans, the math changes significantly.

With the Trump administration capping federal borrowing limits, private lenders are expected to compete aggressively for borrowers. For parents with good credit, private loan rates can range from 3% to 7%, offering a better alternative to the 9% federal Parent PLUS loan plus fees. Experts advise families to calculate total costs, including fees, before borrowing.

Scholarships, grants, and employer benefits should be the first resources exhausted. Financial planning should start early, ideally before college applications, with FAFSA submission as a critical step, as aid is first come, first served.