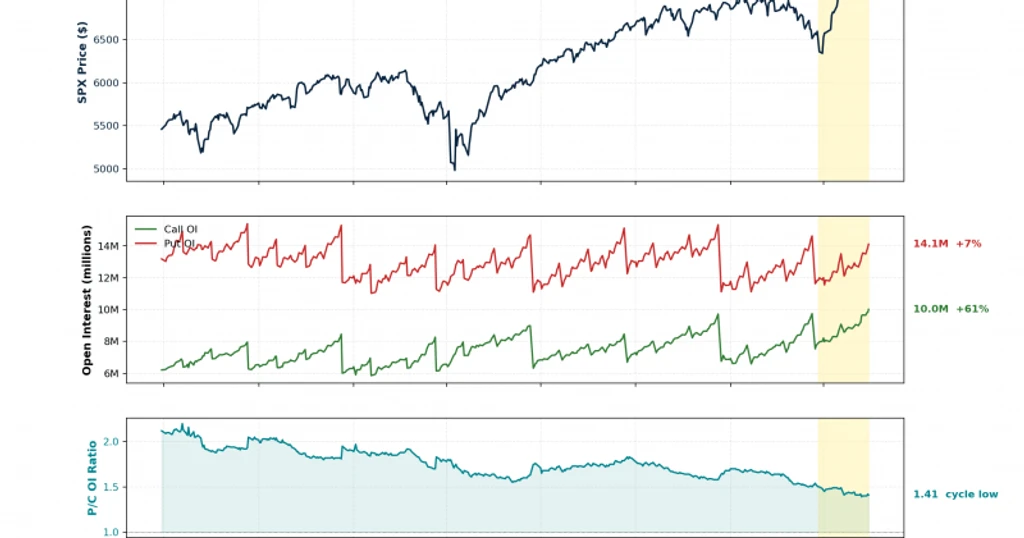

The S&P 500 blew past 6,500 on April 1, adding roughly 100 points in a single session. The engine behind the move was the options market, where a torrent of call buying triggered a textbook gamma squeeze that forced market makers to keep buying stocks.

Options trading volume hit $2.6 trillion in notional value, heavily skewed toward calls.

When traders buy call options, dealers who sell those contracts hedge by purchasing the underlying stocks. The more the stock rises, the more shares dealers need to buy to stay hedged, pushing prices higher still. Dealers were sitting on short gamma positions, and their only rational response was to buy into the rally.

By May 8, net gamma exposure for the S&P 500 reached $107.18 billion. At that level, dealers had shifted to a net long gamma position, which generally acts as a stabilizer. When dealers are long gamma, they sell into rallies and buy into dips, smoothing out volatility.

Two macro factors gave traders confidence to pile into calls: optimism around artificial intelligence and easing tensions between the US and Iran. Corporate earnings added fundamental support.

With dealers now long gamma, price swings should be dampened. But once the current options driving the gamma squeeze expire, the market may be vulnerable to increased volatility if negative developments arise.