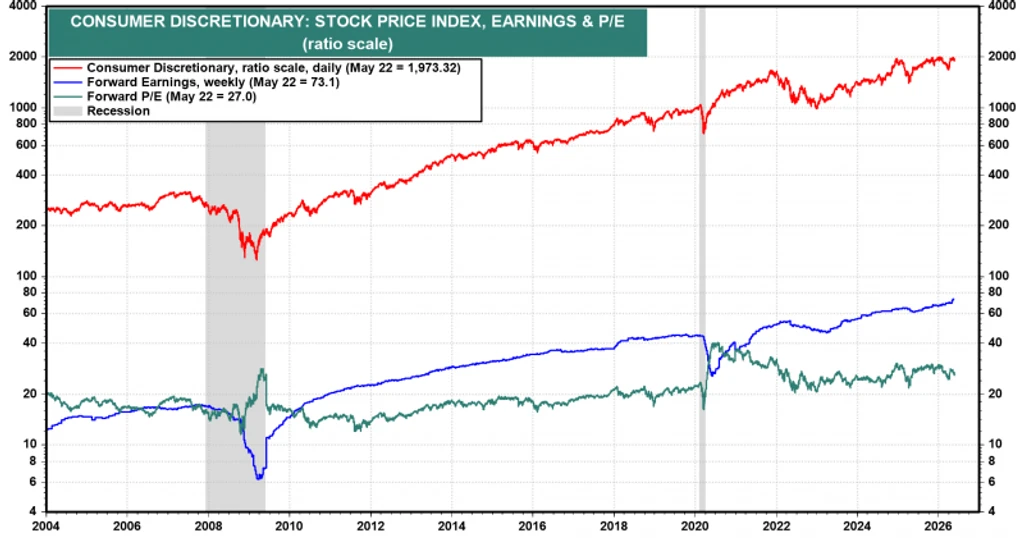

A historic divergence is unfolding on Wall Street. While the S&P 500 climbs, the Consumer Discretionary sector has fallen to its weakest relative position in 20 years. In February alone, these stocks-including major holdings Amazon and Tesla-dropped roughly 5%, even as the broader index held steady. As of mid-May, the sector index hovers near 1,950, a level that signals structural weakness rather than a simple correction.

Amazon and Tesla together account for about 38% of the sector's weighting, meaning their individual struggles can drag the entire category down. The headwinds are clear: shifting tariff policies, persistent inflation, and a softening job market that has created a bifurcated consumer economy. Wealthier households continue spending thanks to asset gains, while lower-income families are pulling back sharply.

Meanwhile, investor enthusiasm has pivoted almost entirely toward AI infrastructure and services. This rotation explains how the S&P 500 can thrive even as a major sector flounders. The index's composition has tilted heavily toward tech and AI names, masking the pain in discretionary stocks.

The risk is concentrated: if the AI trade stumbles, there is no healthy consumer sector to catch the fall.