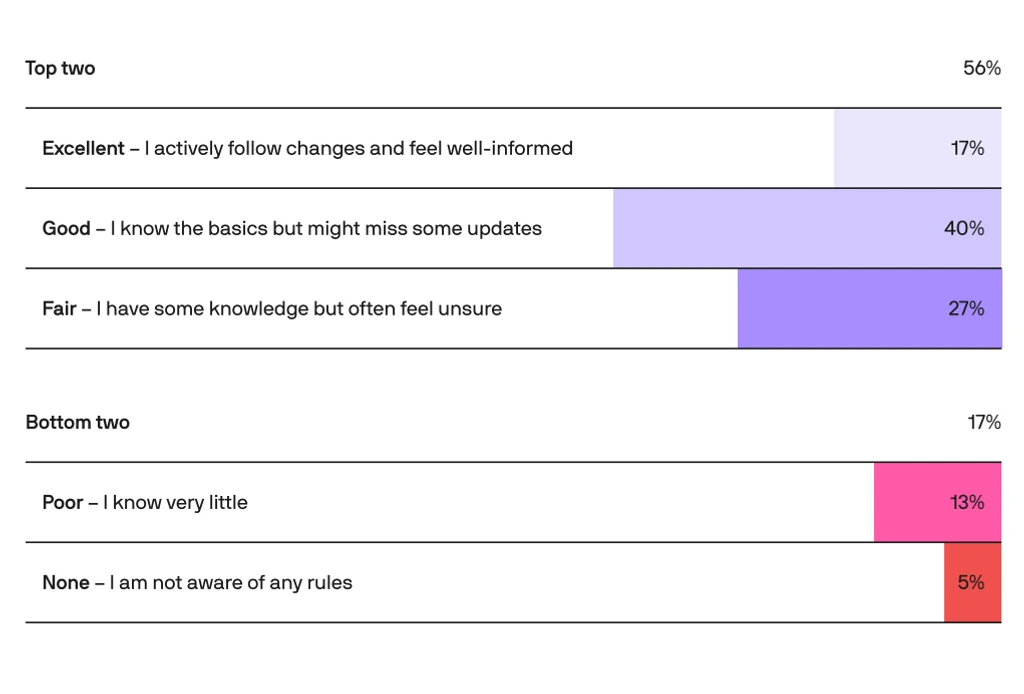

A majority of U.S. crypto users lack clarity on basic tax obligations, according to a new survey by Coinbase and CoinTracker. Fewer than half correctly identified when crypto transactions trigger taxable events.

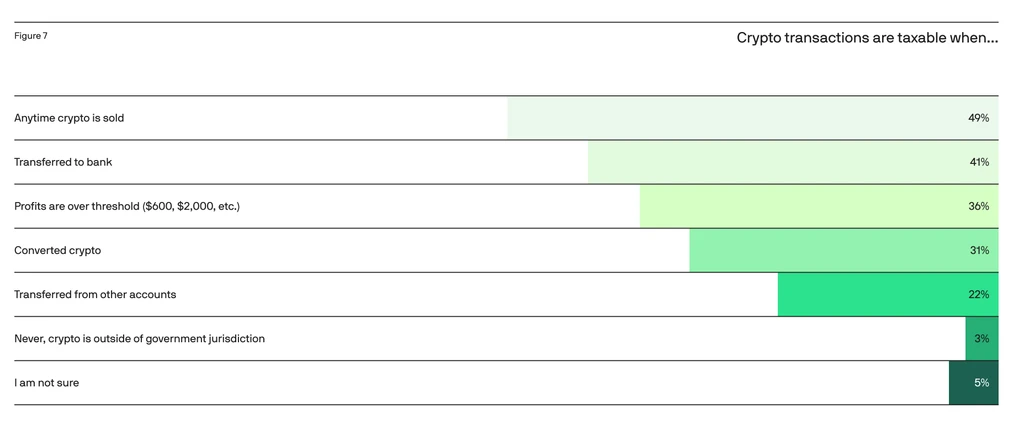

The 2026 Crypto Tax Readiness Report, based on a survey of 3,000 users, found only 49% knew that selling crypto creates a tax liability. Nearly 25% mistakenly believed transferring crypto between wallets triggers taxes.

Despite confusion, most respondents want to comply. Seventy-four percent acknowledged crypto is taxable, and 65% have reported past activity. "This refutes the misconception of widespread crypto tax avoidance," the report stated.

Fragmented asset storage complicates compliance. On average, users maintain assets across 2.5 platforms, with 83% employing self-custody wallets. Tracking cost basis across platforms remains difficult.

Starting in 2025, brokers must issue Form 1099-DA but will not include cost basis data. Investors must reconcile records independently, increasing complexity.

Most users rely on traditional tax tools - 78% use standard software and 52% consult accountants. Only 8% use crypto-specific services. Interest in AI-assisted tax filing is rising, with nearly half open to using AI for calculations.

The IRS recently proposed mandating electronic delivery of tax forms. Exchanges may sever ties with users who refuse digital communications, further pressuring compliance under evolving regulatory frameworks.