Financial exclusion remains a major challenge for governments. Over 1.3 billion adults lack access to a financial account, relying on cash and missing out on economic opportunities. CBDCs, as a trusted, risk-free alternative to physical cash, can bridge this gap by providing seamless entry into the financial ecosystem.

Wider access to financial institutions stimulates economic growth and ensures policy benefits reach all citizens. However, many low-income individuals depend on cash due to its ease of use and lack of transaction fees. This creates a divide between the unbanked and the formal economy.

CBDCs can operate through a two-tier distribution model, allowing both banks and non-banking entities to serve the financially excluded. Offline capabilities are also being developed to ensure accessibility in remote areas with limited connectivity.

As public-sector infrastructure, CBDCs prioritize welfare over profit, offering low transaction costs and enhancing financial resilience. They also enable privacy-preserving data sharing, helping users build credit histories and access financial services.

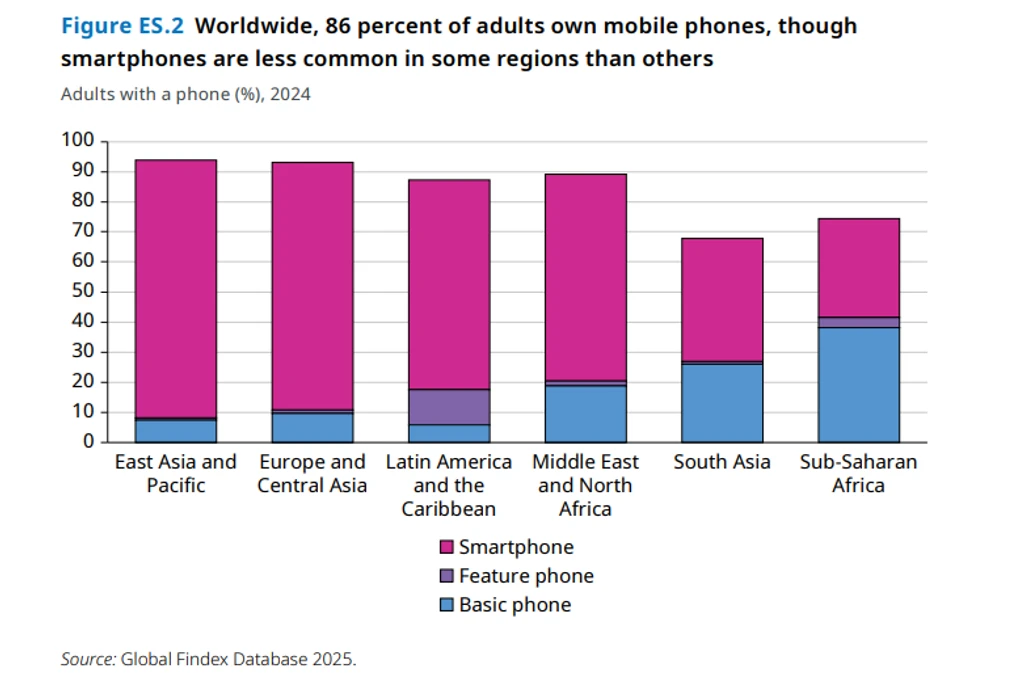

With growing mobile phone ownership and digital payment adoption, CBDCs present a viable solution for expanding financial inclusion globally.