That $87 minimum payment on your credit card statement? It's a trap. Credit card companies engineer these payments to keep you paying interest indefinitely, and it's working: Americans paid a record $160 billion in credit card interest in 2024, with total debt hitting $1.28 trillion, according to the Consumer Financial Protection Bureau and the New York Federal Reserve.

Most of that debt comes from people making only the minimum payment each month. Here's what the banks don't want you to know.

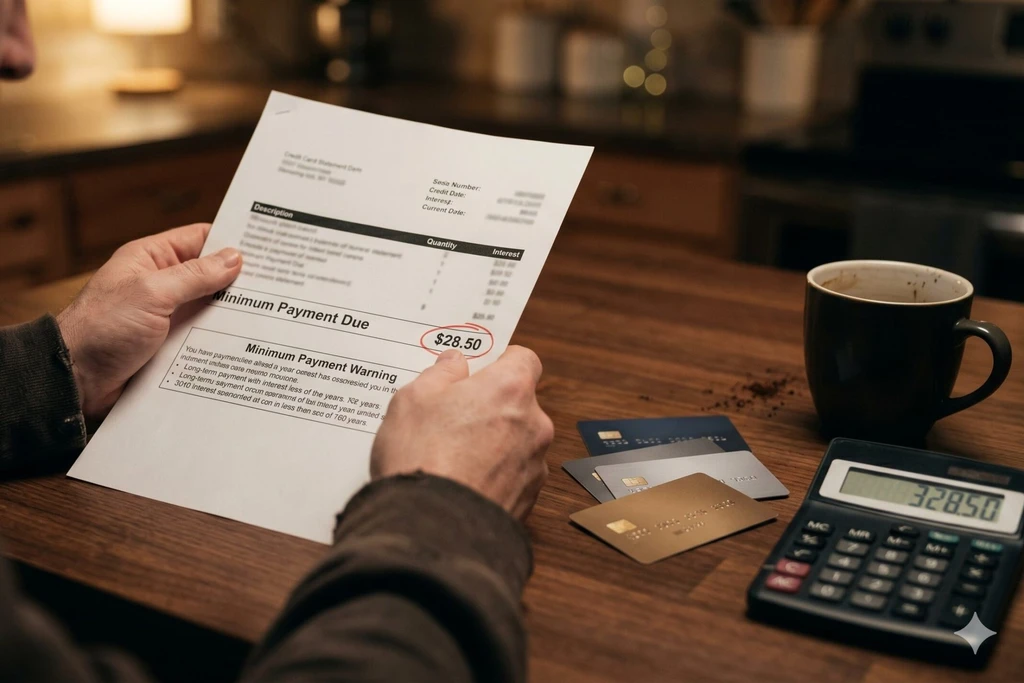

1. The Math Is Rigged

Minimum payments are typically 1% of principal plus interest, or about 2% of the balance. This ensures almost every dollar goes to interest, not principal. A $7,000 balance at 21% APR with a $200 monthly payment takes 4.5 years and costs $4,000 in interest. Pay the minimum, and you're looking at decades.

2. Interest Compounds Daily

Issuers calculate interest using a daily periodic rate (APR divided by 365). Each day, unpaid interest is added to your balance, and you accrue interest on the new total. This is compound interest working against you.

3. You Lose the Grace Period

Carry a balance from one month to the next, and the 21-25 day grace period on new purchases disappears. Every new purchase starts accruing interest immediately.

4. One Missed Payment Can Trigger 29.99% APR

Miss a payment by 60 days, and many issuers slap a penalty APR of 29.99% on your existing balance. This higher rate can stick around indefinitely.

5. Minimum Payments Hurt Your Credit Score

High credit utilization-even with perfect on-time payments-lowers your FICO score, leading to higher rates on car loans, mortgages, and insurance.

6. Persistent Debt Is a Silent Crisis

The CFPB defines "persistent debt" as where half your payments go to interest and fees. In 2024, 13% of cardholders were trapped in this cycle, up from 9.9% in 2022.

7. Every Dollar in Interest Is a Lost Investment

A $6,000-$7,000 balance at 22% APR costs roughly $1,400 a year in interest. Invested in an S&P 500 index fund over 20 years, that would grow to more than $80,000.

How to Escape: Stop using the card. Pay more than the minimum-even $50 extra cuts years off the timeline. Consider a balance transfer to a 0% APR card. Call your bank to ask for a lower rate. Or use the avalanche or snowball method to pay down debt.