Investors are mispricing what one analyst calls a major 'dislocation' risk in perpetual preferred stocks, specifically Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC).

Matt Dines, CIO of Build Markets, says corporate issuers of perpetual preferred stocks never have to repay the principal. They can pay dividends indefinitely, without renegotiating terms. If holders want to cash out, they must sell on the secondary market, exposing them to liquidity contraction and interest rate risks forever.

"If spreads start to rise and the market demands higher yields from corporate borrowers, you also have to attach that to the infinite duration of the perpetual," Dines said. "If this dislocation comes in liquidity, it will come from the fiat side."

The warning comes as STRC sees surging demand. Daily trading volume hit a record $1.5 billion on Thursday as Strategy leans on preferred stock issuance to fund Bitcoin purchases.

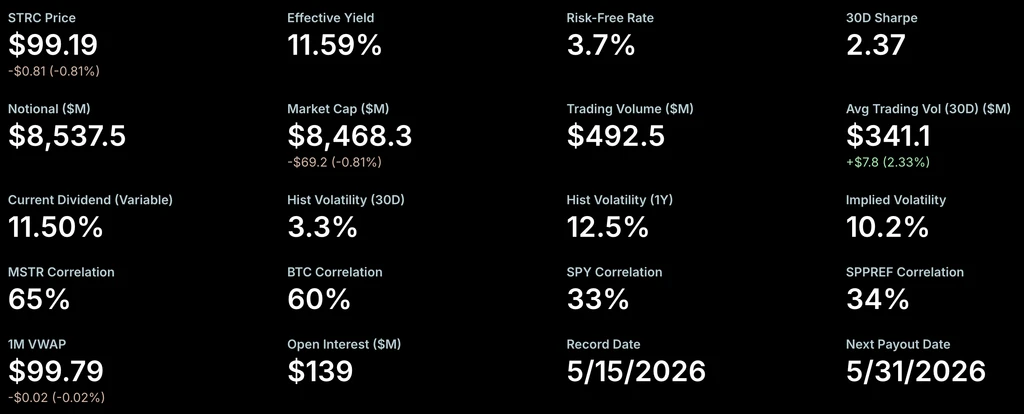

STRC has an authorized issuance cap of about $28 billion, according to Delphi Digital. If the cap is not raised, Bitcoin accumulation may slow. The total notional face value of outstanding STRC shares stands at $8.5 billion, with a market value of about $8.4 billion.

STRC trades near $99 per share with an 11.5% variable dividend rate that can change monthly. Strategy has opened voting for semi-monthly dividend payments.