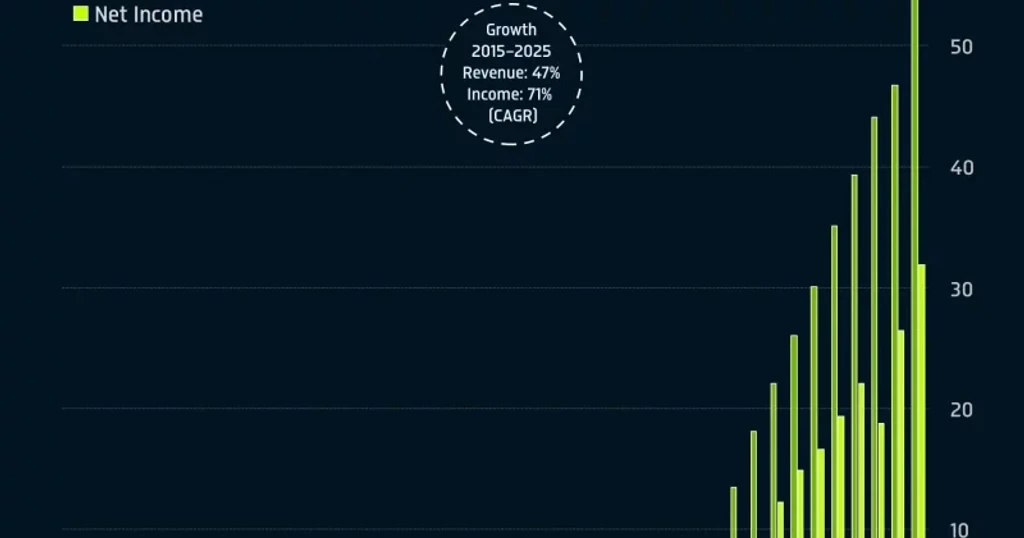

Nvidia posted $81.6 billion in quarterly revenue, an 85% jump year-over-year, driven almost entirely by its data center segment. That division alone generated $75.2 billion. Despite the record, shares dipped in after-hours trading.

Bank of America raised its Nvidia price target from $320 to $350 on May 21, reaffirming a Buy rating and naming the chipmaker a top pick. With shares near $223, that target implies roughly 57% upside.

The company guided approximately $91 billion for the next quarter and authorized an $80 billion stock repurchase program with a higher dividend.

Former Bitcoin miners like Core Scientific and Hut 8 are now leasing GPU capacity to AI labs, leveraging existing energy infrastructure to host Nvidia's data center GPUs. Bank of America's analysts revised estimates for the total addressable market for AI data centers through 2030, underscoring sustained GPU demand.

For investors, Nvidia's earnings cycle signals hyperscaler and AI lab spending on compute, which flows downstream to GPU hosting providers-many formerly Bitcoin miners. Annualized revenue could approach $360 billion. AMD and custom silicon from Google and Amazon remain competitive threats but have not dented Nvidia's market share in training workloads.