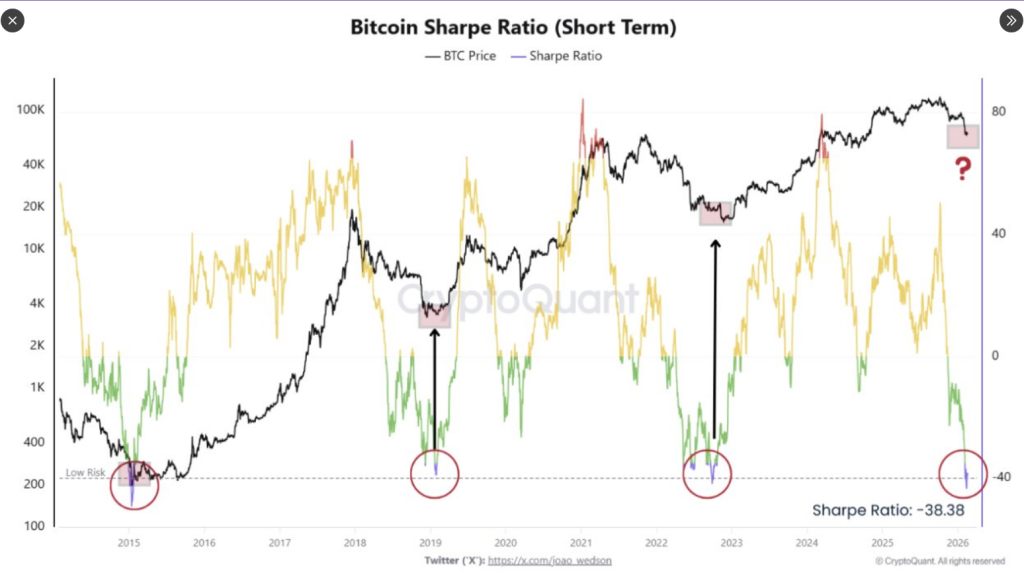

A critical risk metric for Bitcoin has plunged into territory historically associated with major buying opportunities. The short-term Sharpe Ratio has fallen to approximately -38.38, a level rarely observed in the market. Analysts note that similar extreme readings occurred around the market lows of 2015, 2019, and late 2022, periods that subsequently saw substantial recoveries.

The Sharpe Ratio measures investment returns against volatility. A significant negative reading indicates investors have experienced substantial losses relative to market fluctuations. This -38.38 reading is exceptionally extreme, having occurred only a handful of times in Bitcoin's history, each time following periods of high stress and weak sentiment. This pattern suggests that selling pressure may be exhausting, even when market charts appear unfavorable.

Past market cycles provide a framework for interpreting this signal. Previous extreme readings in risk metrics and investor sentiment preceded rallies. These moments, occurring around $287 in 2015, $4,100 in early 2019, and $15,000 in late 2022, were characterized by high trader capitulation, thin trading volumes, and spiked volatility, yet they ultimately led to multi-month rallies.

Bitcoin's price has recently been influenced by broader market sentiment and geopolitical events. While it has shown resilience at times, it has also experienced pullbacks, particularly during periods of reduced liquidity. This volatility has made short-term traders cautious, while long-term investors seek confirmation of fading selling momentum.

While this signal suggests a potential buying zone, external factors like liquidity tightening or macro shocks could prolong downward pressure. The recent decline from an all-time high near $126,200 to approximately $65,700 indicates that a significant portion of the move may be behind us. However, risk management, including position sizing and clear entry plans, remains crucial for investors considering action at these levels.