Regulatory uncertainty around stablecoins could hurt traditional banks more than crypto firms, according to Colin Butler, executive vice president of capital markets at Mega Matrix.

Banks have invested heavily in digital asset infrastructure-but cannot fully deploy it. Their general counsels advise boards to withhold further capital expenditure until regulators clarify whether stablecoins are deposits, securities, or a distinct payment instrument.

JPMorgan built its Onyx blockchain payments network. BNY Mellon launched digital asset custody services. Citigroup tested tokenized deposits. Yet all face regulatory caps on scaling.

Crypto firms operate comfortably in gray zones. Banks cannot.

The yield gap intensifies pressure: stablecoin platforms offer 4%-5% returns; average US savings accounts yield under 0.5%. Depositors moved rapidly to money market funds in the 1970s-today’s shift takes minutes.

Sygnum CIO Fabian Dori says large-scale deposit flight isn’t imminent, but marginal migration is accelerating-especially among corporates and globally active fintech users. Stablecoins must be seen as productive digital cash-not just trading tools-for competitive pressure to peak.

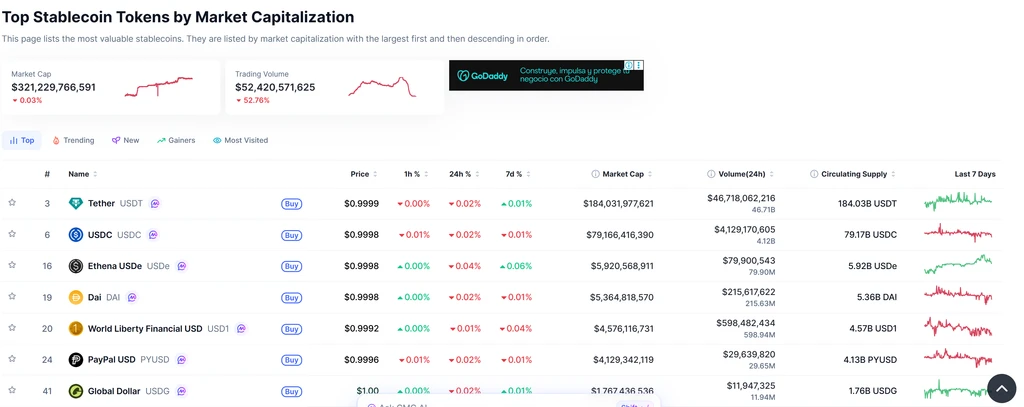

Restricting stablecoin yield could backfire. US law bars issuers from paying yield directly, but exchanges circumvent this via lending and staking. Tighter rules may push capital offshore-to synthetic dollar tokens like Ethena’s USDe, which generate returns through derivatives. That risks shifting capital into opaque, less regulated structures with fewer consumer protections.