China posted its strongest producer inflation numbers in years last month. The April Producer Price Index rose 2.8% year-on-year, handily beating expectations between 1.5% and 1.9%. The Consumer Price Index also came in hot at 1.2%, against forecasts of 0.8% to 1.0%. These numbers end a 41-month deflationary stretch for the world's second-largest economy.

The gains reflect a 14.1% surge in export growth, pumping demand through China's manufacturing base and pulling commodity prices higher. Core CPI landed around 1.1%, suggesting the price increases aren't just about volatile food and fuel.

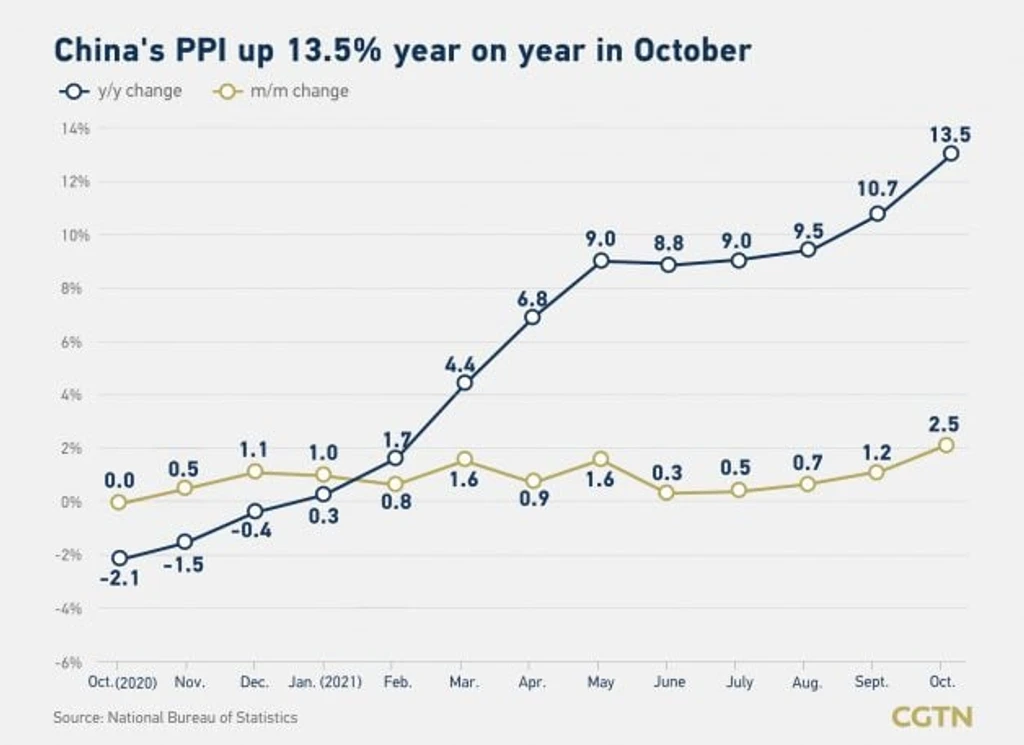

For context, China's PPI had been negative for 41 straight months, a streak that began in late 2022 and became a defining post-COVID economic narrative. That streak is now definitively over.

The implications are global. In the US, the most recent PPI showed a 2.7% reading, which undershot expectations. So the world's two largest economies are sending opposite inflation signals: China running hotter than expected, the US cooler.

If Chinese inflation continues to accelerate, the People's Bank of China has less room for aggressive monetary easing. Rate cuts become harder to justify when prices are already climbing. Meanwhile, the softer US inflation print increases expectations for Fed rate cuts, creating a scenario where the two economic superpowers are potentially moving in opposite policy directions.