Goldman Sachs research highlights an unusual divergence in March 2026: the US dollar index climbed more than 2% as the US-Iran conflict escalated, but Treasuries did not see the typical flight-to-safety bid. Instead, foreign official institutions, including those from China and Japan, were actively selling US government bonds.

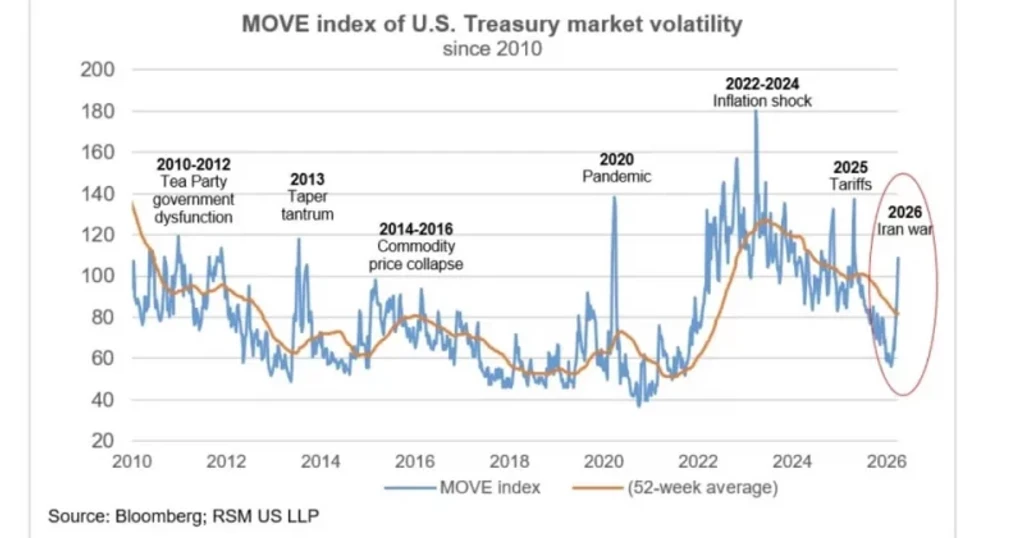

The US-Iran conflict escalated sharply in early March 2026, with disruptions in the Strait of Hormuz creating what Goldman Sachs described as the largest energy supply shock on record. Oil prices surged, and with them came a wave of inflation anxiety that changed the calculus for bond investors. Rising Treasury yields during this period were not a reflection of economic optimism; they reflected fear that inflation, not recession, was the dominant risk.

The dollar, meanwhile, benefited from improved terms-of-trade dynamics. The US remains a major energy producer, so even as global oil supply tightened, the relative economic position of the US strengthened compared to energy-importing nations.

Goldman Sachs identified foreign institutions, notably from China and Japan, as significant sellers of Treasuries. Japan’s selling may be partly driven by the need to defend the yen. China’s motivations include the broader context of US-China tensions and a desire to diversify reserves away from dollar-denominated assets.

Goldman Sachs lowered its 2026 US growth forecast and raised its inflation projections, a combination that has an uncomfortable name: stagflation. The bank also pushed back its expected timeline for Federal Reserve rate cuts from June to September or later, with a new projected terminal rate between 3% and 3.25%.